- Apollo Micro Systems Limited (AMSL) Share Price Target – FY25 Results & Future Outlook

- FY25 Financial Performance – A Strong Year

- Big Move: Acquisition of IDL Explosives Ltd.

- Capacity Expansion: Units 2 and 3

- Fundraising and Shareholding Update

- Order Book and Revenue Guidance

- Strong Program Involvement

- Focus on ‘Make in India’ and Exports

- Managing Working Capital

- Market Outlook and Challenges

- Management Commentary – Tone & Vision

- Analyst View – Apollo Micro Systems Limited (AMSL) Share Price Target

- Apollo Micro Systems Limited (AMSL) Share Price Target – FY25 Results & Future Outlook

- FY25 Financial Performance – A Strong Year

- Big Move: Acquisition of IDL Explosives Ltd.

- Capacity Expansion: Units 2 and 3

- Fundraising and Shareholding Update

- Order Book and Revenue Guidance

- Strong Program Involvement

- Focus on ‘Make in India’ and Exports

- Managing Working Capital

- Market Outlook and Challenges

- Management Commentary – Tone & Vision

- Analyst View – Apollo Micro Systems Limited (AMSL) Share Price Target

Apollo Micro Systems Limited (AMSL) Share Price Target – FY25 Results & Future Outlook

Apollo Micro Systems Limited (AMSL) has drawn a lot of attention after its strong performance in FY25. With a sharp jump in revenue, profit, and a strategic focus on defense manufacturing, AMSL is now seen as a key player in India’s defense sector. This article breaks down their recent earnings, key developments, and what it could mean for the Apollo Micro Systems Limited (AMSL) share price target going forward.

Read More:

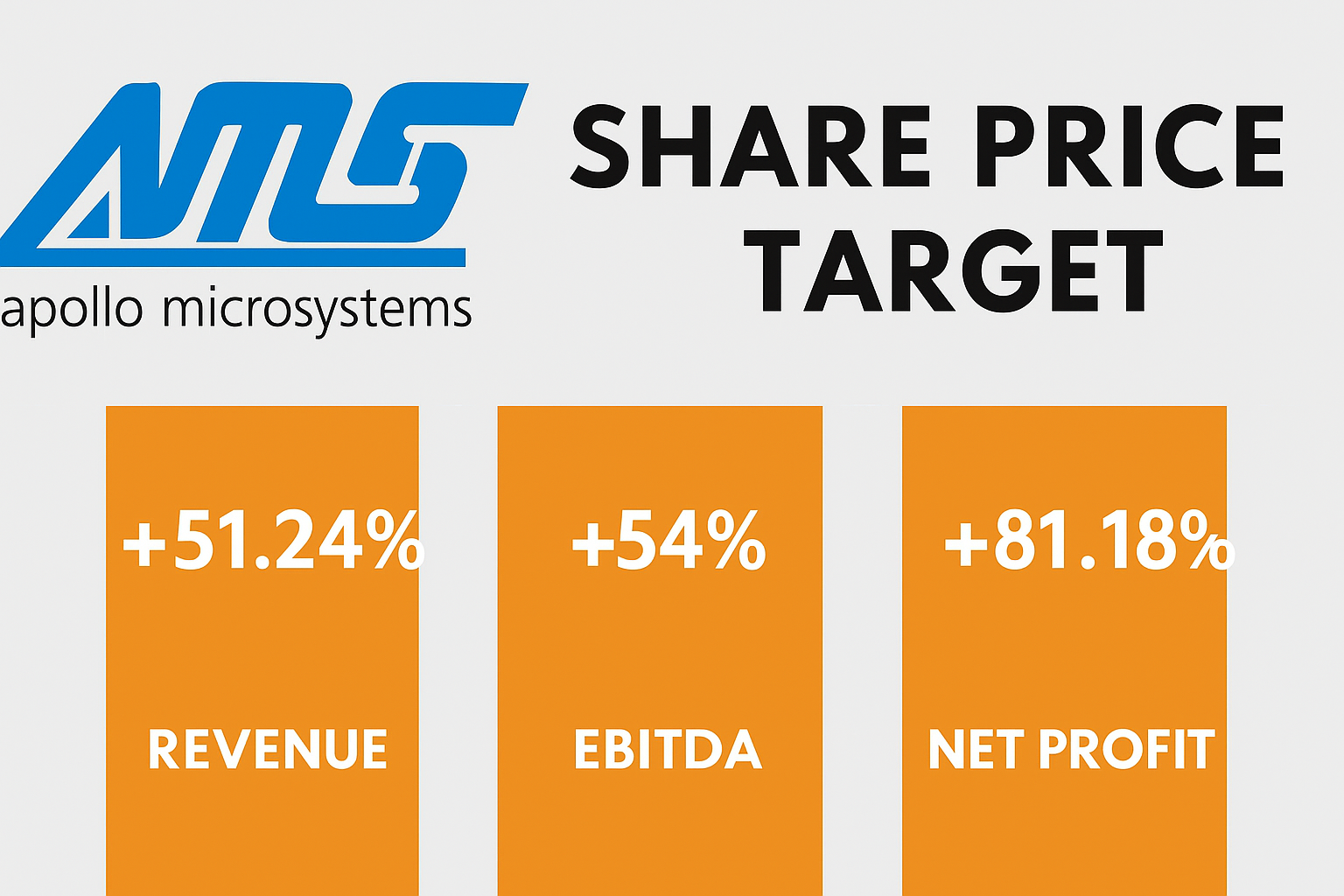

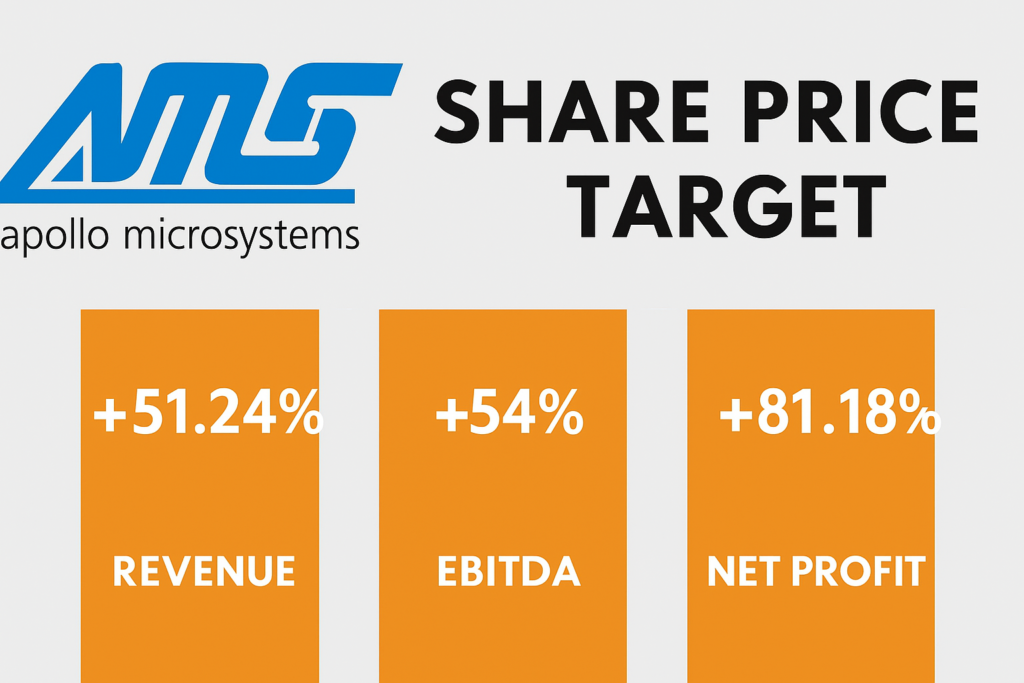

FY25 Financial Performance – A Strong Year

AMSL delivered impressive financial growth in FY25. Here’s a quick look at their numbers:

| Financial Metric | FY25 | Growth YoY |

|---|---|---|

| Revenue | ₹562.07 crore | +51.24% |

| EBITDA | ₹132 crore | +54% |

| Net Profit | Significant Jump | +81.18% |

| EBITDA Margin | 23.5% | — |

In Q4 FY25 alone, AMSL reported ₹162 crore in revenue, up by 19% YoY, and maintained a healthy EBITDA margin of 22%. These numbers were not just ahead of guidance but also showed strong execution.

Key Takeaway

- AMSL beat market expectations.

- Profit margins are stable, which is good for long-term outlook.

Big Move: Acquisition of IDL Explosives Ltd.

One of the biggest developments in FY25 was AMSL’s acquisition of IDL Explosives Ltd.

Why it Matters:

- It adds vertical integration for AMSL in the defense space.

- AMSL is shifting IDL’s focus from mining to defense explosives, which bring better profit margins.

- Though IDL had accumulated losses, AMSL sees this as a benefit due to the tax shield these losses provide.

- AMSL expects IDL to become EBITDA positive in upcoming quarters.

This acquisition is expected to play a key role in expanding the company’s reach in defense manufacturing, further influencing the Apollo Micro Systems Limited (AMSL) share price target in the next 1-2 years.

Read More:

Capacity Expansion: Units 2 and 3

AMSL is investing in new production units to meet growing demand.

Unit-wise Status:

| Unit | Current Status | Full Operations |

|---|---|---|

| Unit-2 | Partial operations started | Q2 FY26 |

| Unit-3 | Production begins in Sep 2025 | Q4 FY26 |

The capital expenditure is happening in two phases:

- Phase 1: ₹150 crore

- Phase 2: ₹100 crore (approx.)

These investments will help AMSL scale up and take on bigger defense contracts, pushing its growth further and likely supporting a higher Apollo Micro Systems Limited (AMSL) share price target over the medium term.

Fundraising and Shareholding Update

To support this growth, AMSL raised ₹816 crore through a preferential issue. The funds will be used for:

- Working capital

- Research & development

- Innovation and new product development

As a result of this issue, promoter shareholding will come down to around 51%. But this isn’t seen as negative since the money is being used for business growth. This also shows transparency in the management’s approach, boosting investor trust.

Order Book and Revenue Guidance

AMSL’s current order book stands at ₹615 crore. And the company expects this to triple by March 2026.

Here’s what the company is guiding for:

| Metric | Guidance |

|---|---|

| Standalone Revenue CAGR | 45-50% (excluding IDL) |

| Consolidated Revenue (FY26) | Expected to double vs FY25 |

| Margins | Improvement in H1 FY26; stable later |

These numbers give a strong base to raise the Apollo Micro Systems Limited (AMSL) share price target for both short and long-term investors.

Strong Program Involvement

AMSL is actively involved in key Indian defense programs, including:

- Missile Systems: Kusha, QRSAM, Akash-NG

- Electronic Warfare and RF/Microwave systems

This program mix is a big reason why analysts are becoming more confident in AMSL’s future earnings. These projects are complex and long-term, and once a vendor is selected, they stay involved for years.

Focus on ‘Make in India’ and Exports

AMSL continues to support the ‘Make in India’ push. The acquisition of IDL Explosives also opens new export opportunities.

Key points:

- Increased localization of defense equipment.

- Export potential is growing in parallel, especially for electronic systems.

- AMSL wants to be seen as a full-stack defense OEM, not just a component supplier.

With global defense spending on the rise, especially in the Indo-Pacific region, export potential will also contribute to raising the Apollo Micro Systems Limited (AMSL) share price target.

Managing Working Capital

Working capital has been a concern for many defense companies, but AMSL is actively fixing this.

- The company expects its working capital cycle to improve by 100 to 120 days starting FY27.

- Efficient use of the recent fundraise will help improve liquidity.

As cash flows improve, AMSL will have more flexibility for R&D and expansion.

Market Outlook and Challenges

The Indian defense market is large and growing. But AMSL’s management is clear: no single company can serve all needs.

Here are the challenges and AMSL’s approach:

| Challenge | AMSL’s Strategy |

|---|---|

| IDL turnaround | Focused shift to defense explosives |

| Supply chain pressures | Building stable vendor partnerships |

| Long gestation of defense projects | Investing in capacity early |

| Funding large capex plans | Using mix of equity and internal accruals |

Despite these challenges, the outlook remains strong due to consistent execution and rising demand.

Management Commentary – Tone & Vision

Management sounded confident and focused. The tone was realistic, not over-optimistic.

Key messages from leadership:

- Orders are coming in, and execution is on track.

- AMSL is transitioning into a fully integrated defense OEM.

- The goal is to be in a unique group of suppliers in India’s defense ecosystem.

Analyst View – Apollo Micro Systems Limited (AMSL) Share Price Target

Considering the strong numbers, high growth guidance, and strategic investments, analysts are now revising their outlooks. Some brokerage houses have raised their share price targets.

Based on current data:

- Short-term Target (6-9 months): ₹100 – ₹120

- Medium-term Target (12-18 months): ₹150 – ₹180

- Long-term Target (2-3 years): ₹220 – ₹250+

These are not guaranteed returns, but they reflect what many investors and analysts expect if AMSL continues to deliver.

FAQs on Apollo Micro Systems Limited (AMSL) Share Price Target

What is Apollo Micro Systems’ main business?

AMSL designs and develops electronic systems for defense, aerospace, and space sectors. They make products used in missiles, submarines, and other defense platforms.

Why is the IDL Explosives acquisition important?

It helps AMSL control more of the supply chain and move into higher-margin defense explosives, making their business stronger and more profitable.

What is AMSL’s current order book?

As of now, it stands at ₹615 crore, with expectations to triple by March 2026.

What is the expected share price target of AMSL in the next year?

Depending on market conditions and execution, analysts expect a target between ₹150 and ₹180 over the next 12 to 18 months.

Is AMSL a good long-term investment?

The company has shown strong growth and is investing in the right areas. If the execution remains consistent, AMSL could be a strong player in India’s defense sector for the long term.

Apollo Micro Systems Limited is no longer just a small defense supplier. With big capex, new unit expansions, and key defense program participation, it is building a strong foundation. The company’s shift to become a full defense OEM, backed by a smart acquisition and focus on exports, sets it apart.

If AMSL continues on this path, improves working capital, and delivers as planned, the Apollo Micro Systems Limited (AMSL) share price target could see significant upward movement in the next few years. Still, investors should watch for consistent execution and timely roll-out of new capacities.

This is a company with a focused management team, strong financial growth, and a solid strategy. And for anyone looking at the defense sector, AMSL is a name to watch.

Read More at sharepricenews.com